This article will compare Simple interest vs compound interest rates with examples. Let’s first understand some basic ideas about simple interest vs compound interest, a formula for easy calculation, and the main differences.

On the way to financial freedom, skills and education are powerful tools that make massive differences between two interest rates. Simply, interest is a vital first step in smart investment portfolios, and understanding how your money works drives financial growth.

Simple and compound interest are two fundamental methods of calculating interest on investments and loans. Simple interest calculations on your initial principal amount make it easy to compute for short-term loans like personal loans. On the other hand, compound interest calculates both interests on the principal and the accumulated interest over the previous decade. It gains higher returns for long-term investments such as mortgages and savings accounts.

This article will teach you everything you need to know about simple interest vs compound interest.

Read also: Simple Interest: Definition with Example, Formula & Benefits

What is simple interest

A simple interest rate is a straightforward method of calculating only the principal amount of a loan. It includes the principal, interest rate, and period of an investment or loan without compounding.

Simple interest does not include any interest of previously earned interest. The types of simple interest that bank pay their customers on saving accounts or earning from a bond. It usually applies to short-term loans.

Read more: APY vs Interest Rate: What are the Key Differences

Simple interest formula

The formula for simple interest is straightforward:

Simple interest calculation is straightforward,

Simple interest= P × R × N

Where: P=Principal, R= Interest rate, N= in years (term of loan)

Let’s an example to represent this concept clearly

You have borrowed $20,000 at an annual interest rate of 5% for the 2 years. Using simple interest, the interest repays would be:

Interest = ($20,000 x 0.05 x 2) = $2,000. There the total amount would be repaid (Principal+Interest), ($20,000+2,000) =$ 22,000

How to calculate simple interest

To clearly understand how simple interest is calculated with simple examples. Logically simple interest depends on 3 variables:

- The amount you deposit (C Capital).

- The time it will take to withdraw (T time).

- The offered interest rate (r %).

Thus, a simple interest calculation that will be received annually will be:

Example of simple interest calculations

If you deposit $1,000, to return in 4 year(s) @ of 3% you will receive an income of:

- 1styear= $ 1,000*0.03*1= $ 30

- 2ndyear= $ 1,000*0.03*1= $ 30

- 3rdyear= $ 1,000*0.03*1= $ 30

- 4thyear= $ 1,000*0.03*1= $ 30

End of 4 years you will gain interest ($ 1,000*0.03*4) = $120, and the total amount will be received(principal+interest), ($ 1,000+$120)= $ 1,120.

Read more: Finance vs Banking: Difference Between Finance and Banking

What is compound interest

Compound interest means the money increases by the same portion each year. It is calculated on the principal amount and previous period accumulated interest and is referred to as “interest on interest.” You can earn interest periodically each month, including earned interest in the past. It can be calculated in different ways, such as per annum, semi-annually, quarterly, or even daily, depending on the terms and conditions of the investment or loan.

Read more: Can you write a check from a savings account- Here’s How?

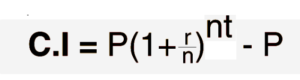

Compound Interest formula

The compound interest calculation formula is:

The compound interest mathematical represents =P (1+rn) nt-P

It calculates total compound interest earned, which interest generated (-) initial principal and total accumulated, including both principal and the earned interest.

Here

- C.I= Compound interest

- P= Initial principal amount

- A= The total accumulated amount

- r= annual interest rate

- n= number of times

- t=time

For example, if you invest $ 5,000 with 3% annual interest rate for 3 years in your savings account, the future value will be: A= $5,000(1+0.03/1) ^(1*3)=$5,459.27

How to calculate compound interest

Compound interest acts like a growing snowball rolling downhill, growing your wealth on both initial principal and accumulated interest, leading to exponential growth over time. The magic of compound interest is that you can take advantage of the returns generated on initial investments and previously accrued interest earned.

Example of how to calculate compound interest

If you don’t withdraw income per period and you let it accumulate to the initial investment amount, the profit will be of compound interest:

- 1st year = $ 1,000*0.03*1= $ 30.00

- 2nd year = $ 1,000*0.03*1= $ 30.90

- 3rd year = $ 1,000*0.03*1= $ 1.82

- 4th year = $ 1,000*0.03*1= $ 2.78

I = $ 1,000*(1+0.03) 4 -$ 1,000= $ 125.5

At the end of the four years of accrued compound interest, you will have the $ 125

I =C*(1+r)- C4 and total will be (Principal+Interest), ($ 1,000+$ 125.5) = $ 1,125.5

Compound interest is more useful when calculating the initial capital that will accumulate at the end of the period, mainly when calculating the amount saved in a few years.

Final capital = C*(1+r) t

Read more: Floating vs Fixed Interest Rate: Which is better for home loan

The Key Differences: Simple Interest vs Compound Interest

When it comes to choosing simple interest vs compound interest, compound interest is beneficial, especially when used for long-term investments.

Compound interest principal grows higher because interest is calculated on the accumulated interest over time, making money faster than simple interest. Compound interest grows better over time and maximizes returns, while simple interest is suitable for short-term loans. Compound interest can affect loans that increase your debt, but simple interest pays less over time if you have a loan.

Simple interest calculates only the principal amount. For example, if you invest $2,000 at a 5 % simple interest rate, you will gain $100 per annum, and after 5 years, your total earnings will be $500. On the other hand, compound interest calculates both principal and accumulated interest. For example, if you invest $1,000 at a 5% interest rate, after 5 years, you gain the interest of $276.28 (approx.).

The basic difference between simple and compound interest lies in how interest is applied and calculated and how it impacts the total amount accrued.

- Simple interest is a straight type of interest and does not consider time. It is calculated only for initial capital borrowed and no reinvestment of earned interest, which means the same percentage of interest, is applied to initial capital for each period.

- While compound interest has a compounding effect over time, this interest results in higher returns. Additionally, it is often considered a decent method because it reflects the time value of money over time and long-term loans or investments.

- In simple interest, if you lend $1,000 at an interest rate of 5% annually for 5 years, you will earn $50 the first year, and after 5 years, it will be $250 in total.

- Compound interest is reinvested along with the principal each period; interest is calculated as an amount that accumulates. For example, if you invest $1,000 at a 5% interest rate per year, you will earn $50 at the end of the 1st year and the total will be ($1,000+$50) =$ 1,050. The 2nd-year interest calculation adds the principal amount of $ 1,000 and 1st-year interest of $50. The result of 2nd year’s interest will total @1,102.50 at the end of the year.

- Simple interest growth interest is the same every period. It is easier to calculate and understand, making it a more accessible method for borrowers and lenders. On the other hand, compound interest calculation is quite hard due to multiple compounding periods. It provides an opportunity to earn a higher return on investment as the interest compounded grows faster over time.

- Simple interest is used for short-term investments, but compound interest is used for long-term mortgages, loans, or investments where interest significantly affects the total amount accrued.

- Simple interest earned only initial principal capital, but compound interest earned both principal and previously earned interest.

- Simple interest usage is in short-term auto loans and bonds, but compound interest commonly uses credit cards, saving accounts, most investment vehicles, mortgages, etc. Typically, banks use compound interest for saving accounts that help users earn more over time due to compounding.

- In simple interest, the time factor plays a smaller role; subsequently, interest is not compounded, but compound interest plays a long duration, a greater effect of compound interest.

- Simple interest provides a stable and predictable return on investment. On the other hand, compound interest gains a higher return due to compounding, but it is less predictable over short periods.

- Simple interest rates apply to short-term and fixed rates, but compound interest applies to long-term investments with variable interest rates. For long-run investments, cumulative interest can generate 50% more earnings than simple interest.

- Simple interest is not influenced by the number of frequent compounding periods, but Compound gain with more frequent compounding results in higher (ROI).

Read more: What are the Key Differences Between Net Salary vs Gross Salary

What is the rule of 72?

The rule of 72 helps estimate how long an investment will take to double if there is a fixed yearly interest rate. It is more accurate for lower rates of return. Divide 72 by investment interest rate, such as if your interest @ is 4%, divide 72 by 4. You get 18, and it will take 18 years to double your investment in value.

Read more: How to Calculate Math of Personal Finance?

The Final Words

Hopefully, familiarizing yourself with the basic concept of simple interest vs compound interest will help you make better financial decisions and boost your net worth over time.

Simple interest offers transparency and simplicity, while compound interest considers the compounding effect over time. Compound interest is more beneficial for long-term growth and maximizes higher return, while simple interest is suitable for short-term investments and loans.

Ultimately, choosing your interest rate and calculation methods depends on specific circumstances, such as the loan term and the desired outcome for both borrowers and lenders.