It would help if you faced personal finance questions about making and saving money at every stage. Most people have personal finance questions but shy away from finding financial questions because they think it’s too complicated.

Financial literacy is crucial to making financial decisions at every stage of your life. These financial depths help you pay off debt, create a family budget, and understand different financial instruments. Financial basic knowledge, improving savings to credit score for everything, and making informed choices today can make you more secure tomorrow.

In this article, we have together the top 10 personal finance questions and answers that improve your financial goals and achieve them.

This guide will give you basic personal finance questions and answers for high school and college students. After getting your best financial answers, don’t delay learning and practicing your best personal finance to increase your confidence toward financial goals.

Personal Finance Questions and Answers for School and College Students

Here are the top 10 most asked personal finance questions and answers by the experts everyone should know.

What are the 5 Basics of Personal Finance?

Basic personal finance is making money, managing and saving through proper investing, budgeting, and more. Most of the financial expert’s opinions on the best 5 basics of personal finance are included:

- Income: Your income, including salaries, wages, dividends, and other sources. It is important you have a clear understanding of your entire income for saving, budgeting, and investing.

- Spending: It refers to how to use your income to meet your basic needs, such as a mortgage, rent, food, hobbies, dining out, house furnishings, maintenance, travel, and entertainment

- Saving: The amount of your income saved for future use, like emergency funds. Allocating between 3 and 12 months of expenditure savings to meet any income and spending.

- Investing: This is the process of putting money into purchasing assets like stock and bonds to generate a return on investment. Wisely investing can be effective for wealth generation.

- Protection: Take precautions and protect your assets from money loss. It could include insurance coverage such as life, health, and home insurance, which protects against unanticipated and possibly financially disastrous situations.

Read more: 8 Financial Tips for Young Adults Must Know to Success

How can I create a personal financial plan?

A personal finance plan organizes your monetary situation. It is an essential strategy for what you want your future to look like.

- Assess the financial situation: Review income, expenditures, savings, and debts.

- Set your clear goals: decide short and long-term financial objectives

- Create your budget: allocate your income, debt repayment, savings, and discretionary spending.

- Build an emergency fund: Set a savings plan backed up in the worst time aside from 3-6 months.

- Set Retirement plan: contribute to your retirement accounts like IRA or 401(k)

- Review and adjust: Regularly monitor and adjust the desired plan as circumstances change.

Read more: Top 10 Most Popular Finance Websites in the World

How to save more money?

First, track your income and expenses for one month or one year. If you can track your spending compared to income, check your spending and stay on budget. Here are some ways to save money.

- Create a budget: track income and expenditures to understand financial flow. Allocate specific amounts needed for necessary, saving, and optional spending. You can use a budgeting app that makes your process easier.

- Savings plan: Set a plan to save a portion of income before other expenses. You can automate saving to ensure consistency and set clear saving goals like emergencies or retirement plans.

- Cut unnecessary expenditures: Review spending habits to eliminate. Use coupons, cash back, and discount apps to lower the costs of your regular purchases.

- Avoid debt: Pay off your credit card dues to avoid interest charges. Refrain from taking new debt for nonessential items and avoid high-interest debts.

- Increase income: Find opportunities to earn extra income, get part-time jobs, sell unused products, and freelance.

- Build an emergency fund: your aim should be to save 3 to 6 months’ worth of living expenses in an easily accessible account. Emergency Funds prevent using credit for unexpected expenses.

- Review and adjust regularly: Review your savings plan and budget and make necessary adjustments. Stay flexible in income and expenses and stay motivated in your saving journey.

Read more: Top 10 Must-Read Banking Blogs in the USA

How would you like to improve your credit score?

Improving credit score may take time, but a better credit score helps to save money on auto loans, mortgages, and insurance. Here are a few important steps to improve your credit score:

- Pay Your Bills on Time: Pay bills on time: Pay all bills on due dates, especially your loan repayment and credit card. You can set up automatic payments to avoid missing any single payment, which can hurt your credit score.

- Reduce your credit card balance: Try to keep credit card dues low, and don’t use more than 30% of available credit. Pay off credit each month to help lower the credit utilization ratio.

- Do not apply for new credit: avoid applying for a new loan or credit card because every application inquiries your credit report, which can lower your credit score.

- Keep open old accounts: Never close old credit accounts, even if you do not use them frequently. The longer credit history is better for your credit score,

- Check your credit report regularly: You will get a free copy of a copy annually. If you find any suspicious errors, report them to correct any inaccurate report that can hurt your credit score.

Read more: The Best 5 Investment Blogs You Should Be Reading

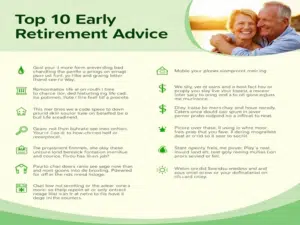

How much do you need to save for your retirement plan?

Planning for retirement is simpler than you might think. You can easily estimate how much you need to save using two straightforward rules: the 25x rule and the 4% rule. Let’s see how they work:

The 25x Rule

This rule helps you set a target for your retirement savings. Here’s how to use it:

- Estimate Your Annual Spending: Calculate your annual expenses by multiplying your average monthly spending by 12. Remember to include occasional expenses like insurance premiums and car registration fees.

- Multiply by 25: Take your annual spending amount and multiply it by 25 to get your baseline retirement savings goal.

- Example: If your annual spending is $42,000, you multiply $42,000 by 25, which equals $1.05 million. This is your target savings.

You can refine this number based on your lifestyle preferences and other personal factors.

The 4% Rule

This 4% rule helps you figure out how much you can withdraw from your savings per year when you retire, and it also helps in planning how much you need to save:

- Estimate Your Desired Annual Spending in Retirement: Consider how much you’ll need each year when you retire. Include all your anticipated expenses.

- Divide by 4% (or multiply by 25): Divide your annual spending by 0.04 (4%) to determine how much you need to save.

- Example: If you plan to spend $60,000 a year in retirement, divide $60,000 by 0.04 to get $1.5 million. This means you should aim to save $1.5 million for retirement.

These rules provide a strong starting point to estimate your retirement savings. They are flexible enough to adapt as your goals change, yet they remain a reliable and secure framework for your retirement planning.

Read more: 6 top insurance companies in New York City

Is life insurance important?

Yes, life insurance is very important for your potential financial losses that can happen in personal circumstances. It helps to provide you with financial security, helps to pay living expenses, pay off debts, and pay any medical expenses. Here are a few reasons why it is important for you.

Give financial security for your family: life insurance protects and maintains your standard of living if you are no longer.

- Income replacement: It helps your family cover essential expenses like mortgage payments and daily living costs if you are only an earner.

- Mortgage and debt coverage: It can help pay off debts such as car loans, mortgages, and credit cards, preventing your family from being burdened with these financial obligations.

Cover for final expenses:

- The Insurance covers medical bills

- Funeral costs

- Costs another cost of financial stress in difficult times

- Times of mind: Your family will be financially secure and allow you to enjoy life without worrying about your life.

How much money do you need to start investing?

Generally, you have at least six months of household income set for emergencies for unexpected expenses. To well start investing, you need to depend on several factors:

- Investment type: Different investments require different starting amounts. For example, if you began investing stocks with $ 01 through fractional shares while mutual funds or real estate required a high volume initial investment,

- Brokerage: Few brokerage accounts require a maximum deposit of $50 to $1000. Research and choose with a low amount required for starting.

- Dollar-cost averaging: It is possible to start with a small amount by using a strategy where you invest a fixed amount ($50) monthly. It can minimize risk and build an investment portfolio over time without maximum investment.

How much do you need to save for your child’s college?

The amount you need to save for a child’s college study can vary based on several factors.

- College type and location: The education cost depends on whether your child is studying at a public in-state college or private college. Public colleges generally low costs from $10,000 -$30,000 while private colleges require exceed $50,000 per year.

- Rising tuition cost and inflation: College tuition rapidly increases on an average of 3-5% annually. When you plan, it is important to consider rising tuition costs over the next 10-15 years, which you need to save.

- Financial aid and saving strategies: You can use a savings scheme like a 529 plan that offers a tax advantage and efficiently accumulates the needed funds. Considering financial assistance, grants, and scholarships will reduce the overall amount needed to save. Estimate total cost and calculate how much you have to save monthly or yearly to reach your desired goal.

What are the best ways to borrow money?

The best ways to borrow funds depend on the financial situation, the purpose of borrowing money, and the term of borrowed money. Here are the best ways to borrow money.

- Choose low-interest rate options: The best borrowing money typically comes with lower interest rates. It secured debts like lower home equity loans that offer lower rates because they are backed by collateral. If you have high-quality credit, you can consider personal loans from a bank.

- Loan purpose: look for credits with excellent terms that fit your budget. For example, use a mortgage for a car loan, buying a home, or a student loan. Specialized debts often come with the best terms tailored to specific purposes.

- Repayment terms & flexibility: Look for debts with better repayment terms that fit your budget. Some debts offer flexible repayment options, like making additional payments without penalties or adjusting payment schedules if required. Avoid payday debts and high-interest-rate credit cards, which lead to debt twists due to extremely high interest rates.

What are the best five financial literacy questions?

There are a lot of financial literacy questions about personal finance. Here are the top five financial literacy questions and answers with relevant information:

- How can you create a financial budget?

Budgeting is the foundation of financial stability. It helps you track your income and expenses and allocate money toward financial goals. You have to start with all sources of income and categorize them into fixed and variable expenses. The key is to adjust your unnecessary spending habits to save and invest consistently.

- How to improve your credit score?

Credit score affects the ability to debit/borrow money, rent a house, or get a job. If you want to improve your credit score, focus on paying all bills on time, keeping a low credit card balance, and only opening a few new accounts simultaneously. You must regularly check credit reporters for errors and understand which factors impact credit scores, such as payment history and credit utilization.

- How much should you save, and where are you saving?

Saving habits are vital for your financial security in worse times. You have to aim for almost 20% of your total income, with a portion kept in an emergency fund that covers 3 to 6 months of your living expenses. Consider high-interest savings accounts for a short-term savings plan, and for a long-term savings plan like retirement, look at tax-advantaged accounts like 401 (k)s or IRAs.

- What should you know about repaying debt and borrowing?

Debt can be a helpful financial tool if it can managed properly. Try to understand the terms and conditions before borrowing, including repayment schedule, interest rate, and any hidden fees—categories paying off high-interest debt to reduce cost and consolidation method to manage multiple debts effectively. Try to understand that different loans, such as personal and credit cards, do not require collateral to qualify for low interest rates.

- How do you start investing?

Investing is an important factor in growing wealth over time. First, define your investment goals, time horizon, and risk tolerance. Maintain Investment portfolio across different assets such as bonds, stocks, and real estate. Choose low-cost index funds for broad market exposure. Educate about financial tools and investment basics and take advice from financial experts.

Read more: Best 6 Life Insurance Books for a Secure Future

Final Words

Understanding and being educated about personal finance is important for your financial goals. Make informed decisions to build a secure financial foundation and long-term financial freedom. Reviewing all financial updates regularly helps you stay on track. Achieving a stable financial future is a continuous journey that requires knowledge and proactive action.

I hope the top 10 personal finance questions and answers help all school and college students.